Not everyone finds themselves paying Moorcroft Debt Recovery, but that doesn’t mean you’ll be as fortunate. Ignoring their letters could lead to more serious consequences down the road. Don’t wait until it’s too late to take action.

In this comprehensive guide, we’ll explain everything you need to know about dealing with Moorcroft Debt Recovery so you can handle the situation and stay on the safe side.

Understanding Moorcroft Debt Recovery

You may be familiar with the name Moorcroft Debt Recovery, especially if you’ve encountered debt challenges.

The experience of receiving constant phone calls and letters can be overwhelming. However, is it as daunting as it appears? Let’s explore further.

What is Moorcroft Debt Recovery?

Moorcroft Debt Recovery is a prominent debt collection agency in the UK, providing services for both consumer and commercial debts.

This organization is legitimate, authorized, and regulated by the Financial Conduct Authority (FCA). Moorcroft was established as a Private Limited Company on March 2, 1983 (Company number: 01703704).

Receiving a letter from Moorcroft indicates that a creditor has engaged their services to recover a debt you owe.

While this may sound intimidating, it’s essential to understand that they are merely fulfilling their role in the debt recovery process. The critical question is: what should your next steps be?

How Does Moorcroft Operate?

Moorcroft Debt Recovery specializes in contacting individuals with outstanding debts, primarily those related to HMRC.

Their methods include sending letters, making phone calls, and even conducting home visits. Their approach is persistent, aiming to ensure that debts are settled.

It’s important to note that once Moorcroft takes over the collection of your debt, payments should be made directly to them, not the original creditor.

However, before you make any payments, consider whether the debt they claim is valid.

Is Your Debt with Moorcroft Valid?

Moorcroft Debt Recovery is not infallible; errors can happen. They may mistakenly contact the wrong individual, or you might have valid reasons to dispute the debt.

If you believe the debt is not yours or is incorrect, you can challenge it. This process may require supporting documentation and potentially professional assistance.

The Human Aspect of Debt Recovery

Moorcroft’s Debt Recovery is not solely focused on collecting debts; it also has a duty to assist individuals facing financial difficulties.

If you demonstrate financial hardship, it can offer guidance and propose manageable repayment plans. Solutions are available, and Moorcroft can help facilitate them.

The pressing question remains: should you pay the debt or contest it? Understanding your options is crucial as we navigate this complex landscape.

Are They an Adversary or an Ally?

Comprehending Moorcroft Debt Recovery’s role is vital for effectively managing your debts.

Although they may initially appear intimidating, ongoing communication can reveal that their goal is to help you resolve your debts and find solutions that fit your financial situation.

Ultimately, whether Moorcroft is perceived as a friend or foe depends on your perspective, knowledge of your rights, understanding of the debt recovery process, and the actions you choose to take.

What’s the Deal with Moorcroft Debt Recovery HMRC debts?

You’ve likely encountered the terms “Moorcroft Debt Recovery” and “HMRC debts” together frequently. Understanding their connection can help clarify the situation.

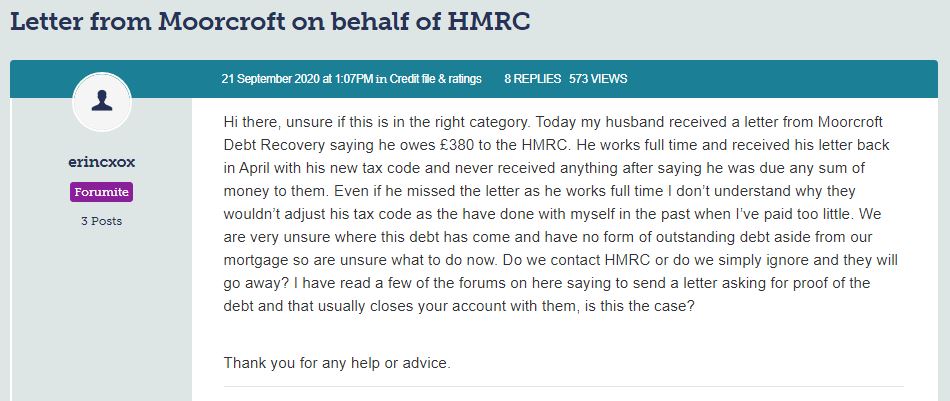

The screenshot below shows a discussion inside a forum where the debtor received a Moorcroft Debt Recovery letter on behalf of HMRC debts.

Source – Money Saving Expert Forum

What is HMRC?

HMRC stands for Her Majesty’s Revenue and Customs, the UK government agency responsible for tax collection. Moorcroft Debt Recovery, on the other hand, is a debt collection agency that operates within the UK.

Moorcroft Debt Recovery and HMRC: A Collaborative Effort

When individuals fail to meet their tax obligations, HMRC does not let unpaid debts linger. This is where Moorcroft Debt Recovery steps in.

They work in conjunction with HMRC to ensure that tax debts are addressed promptly.

How Does Moorcroft Operate?

Moorcroft acts on behalf of HMRC by reaching out to those with outstanding tax debts.

Their methods include sending persistent letters, making phone calls, and occasionally conducting home visits.

While their approach may seem aggressive, it’s important to remain calm; this is part of their standard operating procedure.

If you receive a letter from Moorcroft regarding HMRC debts, you are required to pay them directly. Once Moorcroft takes over the debt collection process, your dealings are exclusively with them, not HMRC.

Validating Your HMRC Debt

Receiving a letter from Moorcroft does not automatically confirm the legitimacy of the debt.

Mistakes can occur, such as contacting the wrong person or administrative errors.

You have the right to challenge the debt if you believe it is incorrect. Always ask for proof when in doubt.

Beyond Debt Collection: Moorcroft’s Role

Moorcroft Debt Recovery is not solely focused on collecting unpaid taxes.

It also has a responsibility to assist individuals who are genuinely struggling to meet their financial obligations.

It can provide advice, suggest manageable repayment plans, and offer support in difficult situations.

Should You Pay or Dispute the Debt?

Deciding whether to pay the amount demanded or challenge the debt is not a straightforward process.

It requires careful consideration of your circumstances. If you find yourself in this situation, it’s essential to navigate it thoughtfully and seek guidance if needed.

Moorcroft’s Debt Recovery: A Friend or Foe?

Moorcroft Debt Recovery may appear intimidating, but they are simply fulfilling their role in debt collection.

They engage with individuals like you daily, working to find solutions for unpaid debts that suit your circumstances.

You have options when dealing with them:

- Negotiate a payment plan

- Challenge the debt if you believe it is invalid

Taking the right steps is crucial. So, what actions should you take when confronted with Moorcroft’s Debt Recovery?

Addressing Moorcroft’s Debt Recovery for HMRC Debts

If you owe money to HMRC and Moorcroft Debt Recovery has contacted you, it’s crucial to address the situation promptly.

Ignoring the issue will only exacerbate the problem. Here’s what you should do next:

- Paying Off the Debt

The most straightforward approach is to pay off the debt in full. Contact Moorcroft, clear the outstanding amount, and you’re done. However, we understand that this may not be feasible for everyone.

- Exploring the Appeal Process

If you’re unable to pay the debt immediately, consider the appeal process. HMRC offers a “Time to Pay” scheme for individuals who cannot clear their debts right away.

When appealing to Moorcroft Debt Recovery for HMRC debts, consider the following:

- Propose a payment plan that spreads the debt over several months, making it more manageable.

However, be aware of the potential pitfalls:

- HMRC may add interest to the total debt.

- The “Time to Pay” option is only available if you can repay the full debt within a year and if the debt is under £30,000.

Carefully consider your options and make an informed decision.

Understanding the Relationship Between Moorcroft and HMRC

The connection between Moorcroft Debt Recovery and HMRC is relatively straightforward.

HMRC often employs debt collection agencies like Moorcroft to recover unpaid taxes. This approach allows HMRC to focus on tax collection while Moorcroft specializes in debt recovery, ensuring efficiency in the process.

Remember, addressing the situation promptly and exploring your options, such as negotiating a payment plan or appealing through the “Time to Pay” scheme, can help you navigate this challenge effectively.

Ignoring the issue will only lead to further complications, so take action now to resolve your HMRC debt with Moorcroft Debt Recovery.

To Sum Up: Moorcroft Debt Recovery HMRC Debt – Pay or Appeal?

In conclusion, whether you should pay or appeal a claim from Moorcroft Debt Recovery regarding HMRC debts ultimately depends on your circumstances.

Here are some key points to consider when making your decision:

- Assess Your Financial Situation: Review your financial situation carefully to determine what you can realistically afford.

- Evaluate Your Options: Weigh the benefits and drawbacks of paying the debt outright versus appealing the claim.

- Make an Informed Choice: Choose the option that aligns best with your financial capabilities and circumstances.

Important Considerations

Initially, HMRC will attempt to recover debts through letters and phone calls or by engaging a debt collection agency like Moorcroft. However, if you continue to ignore their communications, they may escalate their efforts.

If you decide not to pay or cannot afford to, HMRC can employ debt enforcement agents. Therefore, it is crucial not to disregard their attempts to reach you.

They have the authority to recover debts through various means, including:

- Deductions from your wages

- Withdrawals from your bank accounts

- Sending bailiffs to seize your property or valuable items

Always seek professional advice if you are uncertain about your situation or how to proceed. Taking proactive steps can help you navigate this challenging process more effectively.