If you recently received a DCBL letter, you might be feeling anxious or unsure about what to do next. You’re not alone—many people are caught off guard when they get one of these letters.

DCBL (Direct Collection Bailiffs Ltd) is a well-known debt recovery agency in the UK, often seen on TV shows like Can’t Pay? We’ll Take It Away!. But what does it mean when they contact you? And more importantly, do you really have to pay?

Let’s find out.

Who Are DCBL?

DCBL, or Debt Collection Bailiffs Limited, is a leading debt collection and enforcement agency in the UK. As indicated by their name, they engage in both debt collection activities and bailiff operations.

Their debt collection services focus on recovering debts prior to court proceedings. At the same time, their DCBL bailiff operations involve enforcing collections for debts that have been escalated to the High Court and have received a County Court Judgment (CCJ).

Who Does DCBL Chase Debts For?

DCBL does not concentrate on a specific industry; rather, it has expanded its reach to serve a wide array of sectors across the UK.

Their diverse client base includes

- Loan providers,

- Utility companies,

- Banks and,

- Parking firms dealing with unpaid parking tickets.

DCBL is recognised for achieving superior debt recovery rates compared to other firms in the UK, largely due to their integration of modern technology in debt collection and their effective communication strategies with debtors.

Why Is The DCBL Debt Collection Agency Famous In The UK?

DCBL gained significant notoriety through the popular Netflix and Channel 4 program “Can’t Pay? We’ll Take It Away!”

All the High Court enforcement officers featured in this show are affiliated with DCBL, which has contributed to their public profile and recognition.

Why do original debt owners take services from debt collectors like DCBL?

Creditors often become frustrated after numerous unsuccessful attempts to recover unpaid debts.

When debtors consistently ignore outreach efforts from the original creditors, these creditors may turn to debt collection agencies like DCBL to recover their debts.

In some cases, they may even sell the debts to DCBL at a discounted rate, typically between 5% and 20% of the total amount owed. This is when debtors first receive a DCBL letter informing them of the outstanding debt.

What Is A DCBL Letter? Why Are They Contacting Me?

A DCBL letter is a formal notice sent by the agency to inform a debtor of their overdue payments to the original creditor. This letter urges the debtor to settle their debts promptly and outlines potential consequences for ignoring the notice.

If you receive a DCBL letter, it indicates that your original creditor has engaged DCBL to recover the debt after exhausting their own efforts.

Common Communication Methods Used By DCBL

If a debtor continues to ignore the initial DCBL letter, DCBL will persist in their attempts to contact them through various channels, including:

- Emails

- Phone calls

- Letters

- Occasionally, home visits (in extreme cases)

What Is A DCBL Final Reminder Letter?

If a debtor fails to respond to earlier communications, DCBL will issue a “Final Reminder” letter. This letter is sent as a last warning before the original creditor considers legal action.

Often referred to as a Letter Before Action (LBA), this document will indicate that legal proceedings may be initiated if the debtor does not take steps to resolve the matter.

Many debtors may mistakenly dismiss the initial DCBL letter as a scam, but the Final Reminder serves as a critical notification of impending legal action if the debt remains unpaid.

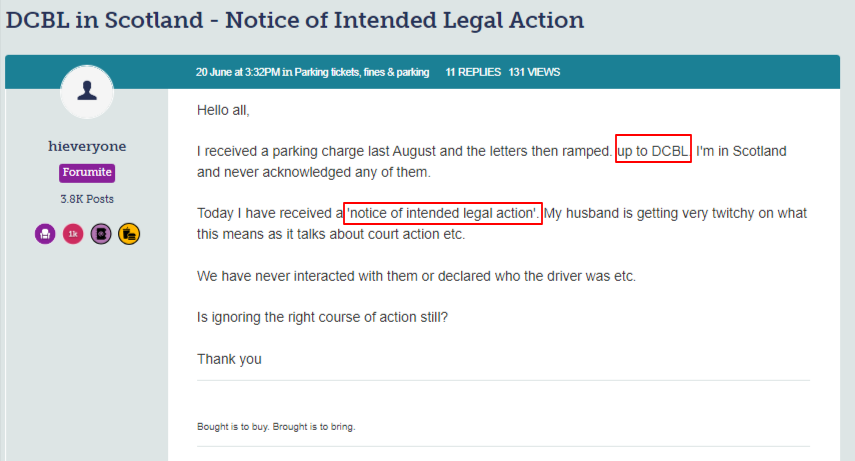

The screenshot below shows someone asking for help from the community to solve this LBO notice from the DCBL firm.

Source: – MoneySavingExpert

Steps To Follow After Receiving A DCBL Debt Recovery Letter And Avoid Litigation

You’re not alone in this situation. Here are some step-by-step instructions to help you effectively address a DCBL debt recovery letter and avoid litigation:

- Avoid Ignoring the DCBL Letter

Ignoring a letter from DCBL can lead to serious legal repercussions. Taking swift action can help you prevent undesirable outcomes.

- Request Proof of Debt

If you have doubts regarding the debt, you have the right to request proof. Always ask for this information in writing and keep a photocopy of your request. DCBL is legally obligated to respond to your inquiry.

- Assess Your Financial Capacity

Once the debt is confirmed as yours, evaluate your financial situation to determine whether you can pay the debt in full or if a manageable payment plan is necessary.

- Negotiate a Payment Plan

Reach out to DCBL to discuss a feasible payment plan that won’t strain your finances. If you’re struggling to negotiate on your own, consider seeking assistance from free charity debt counselling organisations.

The Aftermath: What Happens After Responding To The DCBL Letter?

A proactive response to the DCBL letter shows your commitment to resolving the debt.

However, it’s important to understand that clearing the debt will take time. Remember, every effort counts toward achieving a debt-free status.

Legal Implications: Should I Ignore The DCBL Letter?

DCBL is a powerful agency in debt recovery. Ignoring their letters can lead to serious legal complications.

One consequence may be the original creditor instructing DCBL to initiate court proceedings against you. The worst-case scenario is receiving a County Court Judgment (CCJ), which legally binds you to the debt and negatively impacts your credit score.

Long-Term Consequences: What Happens If A CCJ Is Issued?

If a CCJ is issued against you, your first step should be to agree on a manageable repayment plan.

If you can repay the total amount within the first month, the CCJ can be removed from your credit report.

However, if you only settle the debt after the first month, the CCJ will be marked as satisfied but will remain on your credit report for six years. This negative mark can hinder your ability to secure loans or credit in the future.

What Happens If You Ignore A CCJ?

If you disregard a CCJ, the original creditor may instruct DCBL to take action in the High Court, potentially obtaining a Warrant or Writ of Control to enforce the debt.

You will receive a notice indicating a deadline before enforcement agents (bailiffs) visit your home.

If you ignore this notice, bailiffs may enter your property and seize valuable possessions to recover the debt. These items may be stored until the debt is settled, but they can also be sold at auction if necessary.

Caution

Be aware that additional charges will accrue once enforcement agents become involved. These charges may include:

- Transportation and storage costs for seized items

- Bailiff fees for their time and travel

These extra expenses can add up quickly, making it crucial to act promptly and negotiate before the situation escalates.

Conclusion: The Power Of Timely Action

Receiving a DCBL letter can be stressful, but remember that inaction will only exacerbate the situation.

Taking timely action and communicating effectively with DCBL can help you navigate this challenging period.

This guide aims to empower you with the knowledge needed to handle your DCBL letter effectively. You are now better equipped to take control of your financial situation.

Direct Collection Bailiffs Ltd (DCBL) Contact Details

| Website: | https://dcbltd.com/ |

|---|---|

| The phone number for complaints: | 0203 298 0201 |

| Email address for complaints: | [email protected] |

| London Regional Office: | Solar House, 915 High Road, North Finchley,London, N12 8QJ |

| London Phone Number: | 0203 613 1604 |

| Wales Regional Office: | Sophia House, 28 Cathedral Road,Cardiff, CF11 9LJ |

| Wales Phone Number: | 0292 060 7141 |

| Scotland Regional Office: | Barn Cliuth Business Centre,Town Head Street, Hamilton, ML3 7DP |

| Scotland Phone Number: | 0141 326 0228 |

| Midlands Regional Office: | Colmore Plaza, 20 Colmore Circus,Queensway, Birmingham, B4 6AT |

| Midlands Phone Number: | 0121 581 0957 |

| North West Regional Office: | Direct House, Greenwood Drive, Manor Park,Runcorn, Cheshire, WA7 1UG |

| North West Phone Number: | 01606 361 585 |

FAQs

1. What Is A DCBL Final Notice Of Debt Recovery Letter?

A DCBL final notice of debt recovery letter is a formal communication from Debt Collection Bailiffs Limited (DCBL) that notifies the recipient about an outstanding debt. This letter indicates that the original creditor has engaged DCBL to take action on their behalf to recover the unpaid amount.

2. Should I Ignore A Letter From DCBL?

No, it is not advisable to ignore a DCBL letter. Such a letter is considered a ‘notice of enforcement,’ and neglecting it may result in bailiffs visiting your home within seven days. Involving bailiffs can lead to additional charges on top of the original debt, making it crucial to address the letter promptly to avoid further complications.

3. Should I Pay A DCBL Letter?

If DCBL can substantiate the debt, it is advisable to pay it to prevent legal action. However, if you are unable to pay in full, it is important to communicate with DCBL to arrange a payment plan that is manageable for your financial situation. You are not obligated to pay unless a court order has been issued mandating payment, provided DCBL cannot prove the debt.

4. How Do You Handle A DCBL Letter?

To effectively manage a DCBL letter, follow these steps:

- Identify the type of letter received, whether it’s a Letter Before Action or a Notice of Enforcement.

- Do not ignore the DCBL letter.

- If uncertain, request proof of the debt in writing.

- Assess your financial situation to determine your ability to pay.

- If you can pay, settle the debt. If not, contact DCBL to negotiate a feasible payment plan.

- Verify the authenticity of the letter by checking DCBL’s official contact details on their website.

5. What Happens If I Don’t Pay DCBL?

- If you fail to pay a debt that has been proven to be yours, DCBL will likely pursue legal action, resulting in a County Court Judgment (CCJ). This judgment makes you legally responsible for the debt and negatively impacts your credit history, being recorded in the public register.

- If you settle the debt within the first month of receiving the CCJ, the court may discharge the judgment, removing it from your credit record. However, if you take longer than a month to settle, the CCJ will be marked as satisfied but will remain on your credit report for six years.

- If you continue to ignore the CCJ, DCBL and the original creditor may return to court to seek enforcement through bailiffs, who can visit your home to seize valuable possessions to recover the debt.

6. Is DCBL High Court Enforcement?

No, DCBL is not a High Court enforcement agency. However, it does employ enforcement agents who can act on its behalf. To utilise these agents, DCBL must first obtain a court order against the debtor from the High Court.