Are you struggling with JCIA debt and not sure what to do next? You’re not alone. Managing debt can be confusing, especially when you’re dealing with an organization like JCIA.

If you’re wondering how to handle your JCIA debt in 2024, this article is here to help. We’ll walk you through everything you need to know, from understanding your options to taking the right steps to manage your debt. Let’s make it a little easier to get back on track.

What is JCIA?

JCIA Debt refers to outstanding amounts owed to Jefferson Capital International Acquisitions (JCIA) LLC, a prominent debt-purchasing company.

They typically acquire debts from various businesses, including credit card companies and insurance providers. Once JCIA purchases a debt, they begin their pursuit for debt collection.

JCIA aims to bid as low as possible when acquiring debts from other debt-selling companies. This strategy allows them to generate substantial profits if the debtor chooses to repay the debt.

To illustrate how JCIA makes money by purchasing debts at a considerably lower value than the actual value, consider the following simple scenario:

Assume you have a $100 debt with Company A. JCIA then purchases this debt from Company A for $70. If you ultimately pay your debt in full to JCIA, their total profit from this hypothetical scenario would be $30.

By lowering the debt purchase value, JCIA increases its chances of earning a significantly higher profit when acquiring debts from its debtors.

The Legitimacy of JCIA: Is JCIA a legitimate business?

Concerns and skepticism often arise when contacted by debt-purchasing companies like JCIA.

Their primary methods of communication include:

- Letters

- Emails

- Phone calls

This leads to important questions:

- Is JCIA a legitimate company?

- Are they legally allowed to demand repayment for the debts they have acquired?

These are valid concerns that deserve attention. Let’s take a closer look at this issue.

Is JCIA A Recognised Entity

You can rest assured; the answer is a clear yes.

JCIA operates in full compliance with the regulations set by the Financial Conduct Authority (FCA) in the UK, which provides substantial legitimacy to its operations.

Additionally, JCIA is recognized as a member of the Credit Services Association (CSA), placing it among other reputable debt-purchasing companies.

Regulation Compliance: A Priority for JCIA

When it comes to adherence to regulations, the answer is a definitive yes.

JCIA is regulated by the Financial Conduct Authority (FCA), a UK governmental body that aims to protect consumers, maintain the stability of the financial industry, and promote healthy competition among financial service providers.

Compliance with FCA regulations ensures that JCIA follows fair practices when dealing with customers, further solidifying its legitimacy.

The FCA’s oversight helps to create an environment of trust and accountability in the financial sector.

The Role of the Credit Services Association

As a member of the Credit Services Association (CSA), JCIA adheres to a code of conduct that promotes best practices within the industry.

The CSA encourages and guides its members, including JCIA, to conduct their operations lawfully.

Some key practices that the CSA expects from its members include:

- Transparency: JCIA is committed to providing clear and honest communication with its customers, ensuring they understand their rights and obligations.

- Ethical behavior: JCIA operates with integrity and professionalism, treating customers fairly and with respect.

- Respect for customer rights and needs: JCIA recognizes the importance of understanding and accommodating the unique circumstances of each customer, offering tailored solutions where possible.

So, when you ask, “Is JCIA doing the right thing?” the answer is a resounding yes. By adhering to the regulations set forth by the FCA and the CSA, JCIA demonstrates its commitment to responsible and ethical debt collection practices.

Understanding the Functioning of JCIA Debt: What is a JCIA Debt?

You may be asking, “How does a debt-purchasing company operate?” Understanding this is essential for grasping the concept of JCIA Debt.

JCIA acquires debts from various businesses, which can include:

- Unpaid gym fees

- Outstanding credit card balances

- Telecommunications bills

- Payday loans

- Insurance premiums

These companies sell your debts to JCIA at a fraction of their actual value, marking the beginning of what is known as JCIA Debt.

JCIA’s Commitment to Debt Recovery

“Will JCIA stop at nothing to recover debts?” While it is indeed their business to pursue debt recovery vigorously, JCIA is also bound by regulations and ethical guidelines, which means they cannot overstep certain boundaries.

They are permitted to:

- Send letters

- Make phone calls

- Arrange payment plans

The Interplay Between JCIA and CARS Debt Recovery

You may one day receive a call or letter from an entity known as Creditlink Account Recovery Solutions (CARS).

Confused? Don’t be. CARS is a subsidiary of JCIA and is primarily tasked with locating debtors and facilitating their repayment process.

However, they are prohibited from using intimidation tactics to coerce payment. Always remember your rights, and seek advice if you ever feel pressured.

Continue reading the post to find reviews from debtors about their experiences with JCIA.

Is Your JCIA Debt Valid?

If you’re wondering whether you should pay a JCIA debt, it’s crucial to verify the legitimacy of the debt before taking any action. Here’s how to approach this critical stage:

Step 1: The JCIA Debt Letter

Have you received a debt letter from JCIA or CARS (their recovery arm)? If so, don’t rush to make a payment.

Your first step should be to ensure the JCIA debt is rightfully yours. You can do this by requesting proof of the debt in writing.

Step 2: Requesting Proof of JCIA Debt

JCIA, like any debt-purchasing company, is obligated to provide evidence of the debt you supposedly owe. This proof may come in the form of a credit agreement or a contract you originally signed with the creditor.

Request this proof in writing as your initial response to the JCIA debt letter. Remember, you are not required to pay until they have substantiated the debt.

What If Evidence Isn’t Provided? : Should you pay JCIA debt?

If JCIA fails to provide the necessary proof, you can hold onto copies of their letters, as they may be useful later. However, consider maintaining a record of their inability to produce proof.

Step 3: Failure to Provide Proof: Your Next Steps

You might be tempted to ignore future letters if JCIA is unable to supply evidence of your debt.

However, keeping a record of their failure to provide proof can be beneficial if the matter proceeds to court.

Step 4: Taking Matters to Court: A Possible Scenario

If JCIA decides to take you to court over the debt, having asked for proof and not received it can work in your favour. Presenting evidence that you requested proof and didn’t receive it can potentially help you win the case.

Is there A Potential loophole to avoid JCIA debt?: Statute-Barred Debt

In the UK, some debts become too old to pursue legally after six years, categorizing them as “statute-barred” debts.

You can inform JCIA that you won’t be paying because your debt falls into this category. However, keep in mind that your credit score can still be affected by unpaid or statute-barred debts.

Debunking JCIA Debt Claims

The onus lies with JCIA or CARS to furnish proof of your debt. You are under no obligation to make a payment until you receive a copy of your signed original credit agreement or contract. Remember, you have the right to ask for this evidence!

Some Reviews and forum discussions about JCIA and CARS Debt Collect

JCIA and CARS have received numerous negative reviews online. Many reviewers have voiced complaints about being pursued for debts they believe they are not responsible for and experiencing harassment.

Here are a few examples that highlight this sentiment:

Some Google Reviews Illustrating JCIA’s Operations

- One user reported that Jefferson Capital has been deducting £50 a month from their bank account to settle a £1,900 debt. With less than £200 remaining, Jefferson Capital stopped the deductions to pursue legal action, adding court fees and potentially garnishing wages.

“

For four years, Jefferson Capital has been taking $50 a month out of my bank account to pay off a $1900 debt. With less than $200 to go, Jefferson Capital decided to stop going into my account so they could go after me, legally add court fees and garnish my check… When I called Jefferson Capital to ask them why they were doing this, they replied as they went into my bank account 3 consecutive months, and that was insufficient funds …. Read more.

”

- Another reviewer mentioned having a receipt showing a balance of £0 from Verizon, stating that Jefferson Capital showed no interest in resolving the debt.

“

I have the actual receipt of my final transaction with Verizon, and it shows a balance of $0. I have sent this information to Verizon, as well as another debt collector, before this one. Jefferson isn’t interested in actually settling the debt… Read More

“

Forum Discussions Regarding JCIA and CARS

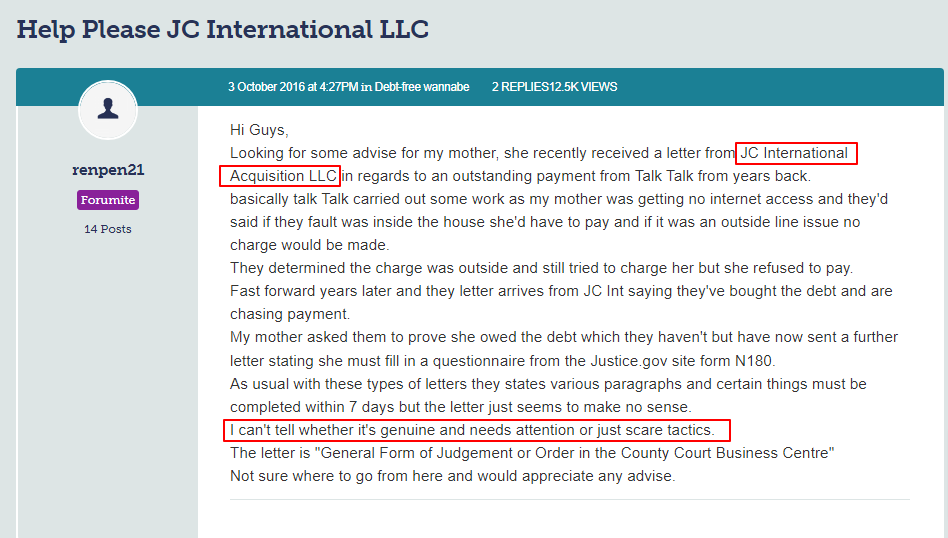

- User renpen21 is seeking help on the forum about JCIA firm – (Source – Money Saving Expert/Forum)

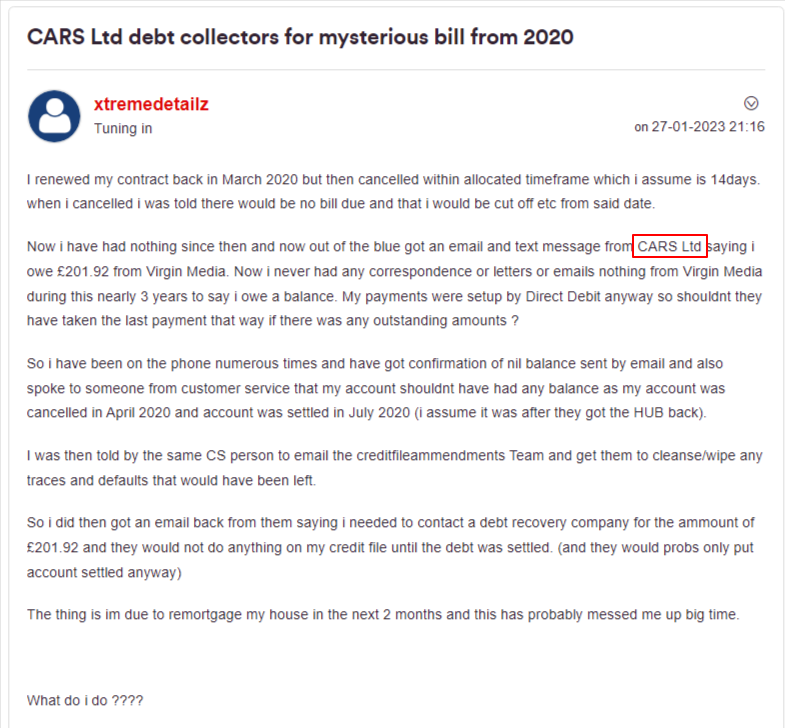

- User Xtremedetailz is seeking help on the forum about the CARS firm (source – virginmedia.com/community)

Dealing with Other Debt Collectors

It’s important to review any outstanding debts you may have with other companies or debt collectors. Here are four steps you can take to stay ahead of potential debt issues:

- Check Your Credit Report: Make it a habit to review your credit report at least once for any defaulted debts.

- Stay Alert for Communications: Be aware of any emails or letters regarding payment reminders or notices.

- Examine Court Records: Carefully read any court records (CCJ records) filed against you.

- Review Your Bank Statements: Check your bank statements to identify other debt collectors and verify if anyone else has purchased your debts.

There are numerous debt collection agencies operating in the UK, but they do not all focus on the same types of debts or work with the same creditors.

By following the steps outlined above, you can reduce stress and potentially save a significant amount of money.

How can I contact JC International Acquisitions (JCIA)?

Knowing how to contact JC International Acquisitions (JCIA) can be extremely helpful. If you need to reach out to JCIA, here is their contact information:

| Phone: | 0203 437 0310 |

| Post: | JC International Acquisition, LLC5th Floor, MidPoint, Alencon Link, Basingstoke RG21 7PP |

| Email: | [email protected] |

| Website: | https://www.jcia.co.uk/ |

Remember, effective communication is essential when dealing with any debt situation.

FAQs

1. How does JCIA chase debtors like you for payment?

JCIA may contact their debtors directly, but it is more likely that CARS – Creditlink Account Recovery Solutions (a part of JCIA) will reach out to debtors in the UK.

CARS is responsible for tracing debtors and facilitating payments. They will send letters requesting payment or contact you to discuss payment plans. These letters may be intimidating and could imply that legal action will be taken if you do not pay.

2. How do you verify debt?

To verify the debt, send a letter to JCIA stating that you dispute the validity of the debt and request a written document confirming that the JCIA debt is indeed yours to pay.

Additionally, ask for the name and address of the original creditor. You are not obligated to pay the JCIA debt until JCIA provides this evidence.

3. What should I do if JCIA contacts me regarding a debt?

Do not ignore communications from JCIA regarding a debt. Request evidence that substantiates your obligation to pay.

You may choose to disregard future letters until they provide legitimate proof. Keep a copy of the letter you sent to JCIA asking for evidence, as it can be used in court if they fail to respond before the court date.

4. Who does Jefferson Capital collect for?

JCIA (JC International Acquisitions) does not collect debts for other businesses. Instead, they purchase debts directly from companies such as gyms, telecommunications providers, credit card companies, payday loan providers, and insurance businesses at a discounted value.

Consequently, the ownership of the debt transfers to JCIA (Jefferson Capital) LLC, meaning the debtor must now deal with JCIA debts rather than the original creditor.

5. Where can I get further help regarding JCIA debt?

Here are some organizations that provide additional support and guidance regarding JCIA debt in the UK:

- Citizens Advice

- PayPlan

- Community Money Advice

- StepChange Debt Charity

- MoneyPlus Advice

- Money Wellness

- Debt Advice Foundation

If you have further financial concerns, it is advisable to consult these organizations for assistance.