Yes, by law, you are required to repay any extra funds you received from your Student Loan Company, as these are classified as Student Loan Overpayment. Ignoring this obligation isn’t an option, but tackling it doesn’t have to be overwhelming.

In this article, we’ll guide you through the steps to address this issue effectively, helping you navigate the repayment process with confidence.

Who is a Student Loan Company, and what are Student Loans?

You may have numerous questions regarding the repayment of your Student Loan Overpayment.

Common concerns include:

- Do I need to repay the entire amount?

- What are the consequences of refusing to repay the overpayment?

- What actions will the Student Loan Company (SLC) take if I do not pay?

- How does this relate to the issue of student loan overpayment?

Firstly, receiving a letter from a Student Loan Overpayment debt collection agency requesting repayment of excess funds should not alarm you.

You are not alone in the UK; many individuals have received similar letters asking for the return of overpaid funds. Additionally, numerous UK residents are seeking assistance online through forums to address this issue.

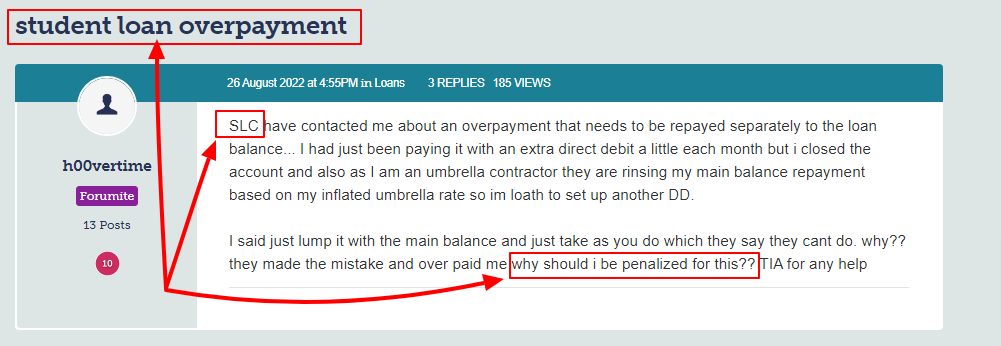

Below is a screenshot of the User “h00vertime” seeking help from the Money Saving Expert – Forum.

Therefore, let us help you deal with this problem properly.

The Student Loans Company (SLC) is a branch of the UK government that provides loans and grants to students for their university or college education.

The SLC is also tasked with collecting loan repayments from students, but this obligation only begins once students enter the workforce.

It’s important to note that you are not required to start repaying your loan immediately upon securing a job. Instead, repayment is expected only after you begin earning above a specified income threshold.

Grants provided by the SLC do not need to be repaid, as they are awarded based on an assessment of the financial circumstances of the student’s parents or guardians.

As the primary entity overseeing the disbursement of student loans and the collection of repayments, the SLC plays a vital role in financing higher education. However, if it is determined that you have received an overpayment, further considerations will follow.

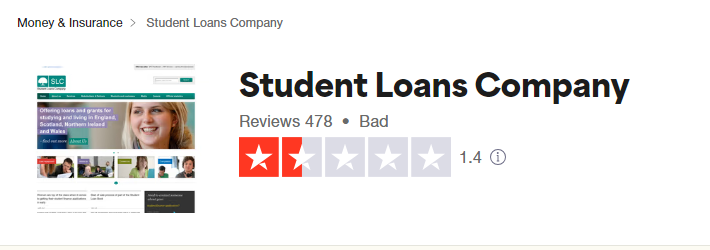

Student Loan Company Reviews

Here are some reviews sourced directly from the Trustpilot website regarding the Student Loans Company (SLC).

These reviews provide insight into how the SLC manages its operations and adheres to its code of conduct.

We will include links to these reviews so you can explore them yourself later.

Their overall Trust Pilot Score is 1.4 out of 478 votes.

- User Yasmine Ait-Abbou has said,

“Mistaken debt, chasing debt with numerous calls

They mistakenly gave me an overpayment – which at the time I was entitled to. 1 year later they have given me numerous calls to pay the debt back, I set up a payment plan (after 2 advisors disconnected me – and I had to call back).

A month after I set-up the payment plan, I received another call – requesting for me to pay the clear the debt. Informed them I had already set-up a plan, and they then chased for the direct debit that didn’t go through, that ended up being a system error on their side.

Mess of a company that continuously punish ex-students for their own mistakes and lack of process.”

Date of experience: June 13, 2023 : (Source link here)

- User Matthew Brindle has said,

“The worst communication I’ve ever known.

Student loans have the absolute worst communication I’ve experienced. Every single time I call up I have to explain the same situation (with no notes on my file) so it’s starting from scratch ever phonecall.

There’s no one there to take ownership of mistakes and you’d be lucky to actually speak to someone in the first place. Awful company I honestly hope they liquidate.”

Date of experience: March 28, 2023 : (Source link here)

Understanding What is Meant by Student Loan Overpayment?

“Student Loan Overpayment” refers to a situation where the Student Loans Company (SLC) has disbursed more funds to you than you are entitled to receive.

This can happen for several reasons, including:

- Changing your course of study

- Modifying your living arrangements, especially if you have children or have moved back in with your parents

- Transferring to a different university

- Discontinuing your studies midway after having received a loan for the term

The most frequent cause of receiving a student loan overpayment notice in the UK is the premature discontinuation of studies.

Interestingly, the overpayment is not always your fault.

There are cases where students who have completed their degrees end up overpaying within a tax year. In such situations, the SLC typically returns any extra payments, but you can also inform them if they do not reach out to you regarding the overpayment.

Does student loan overpayment impact your credit score?

The straightforward answer is no; there is no direct link between student loan overpayments and credit scores.

However, there is a caveat: the debt collection process can have indirect effects, even though overpayment itself does not directly influence your credit score.

Does that sound concerning? Don’t worry! We have you covered.

Do I have to pay back student loan overpayment?

Yes, you are legally required to repay the student loan overpayment in addition to your regular student loan payments. This is the reality you must face.

Repayments are still due on time, even if the overpayment was not your fault initially.

While this may feel somewhat unfair, there is a silver lining: you are permitted to pay back the overpayment in instalments over several months.

Do I have to pay back student loan overpayment if it wasn’t my fault?

Yes, you are still required to repay the student loan overpayment, regardless of whether it was your fault. Receiving an overpayment does not leave you without options.

Student Finance is generally flexible, allowing you to negotiate repayment terms that align with your financial situation.

But what if you’re genuinely struggling to make ends meet? Are there any alternatives available?

Yes, there are solutions to address this issue. So, keep reading to learn more.

Procedure for Repaying a Student Loan Overpayment

Here’s a concise overview of the procedure for repaying a student loan overpayment:

Repayment Options

- If you are still receiving student loan payments, the overpayment can be deducted from future disbursements.

- You can choose to repay the overpayment separately from your regular student loan payments.

- If you are no longer receiving student loan payments, the overpayment must be made as a lump sum or in installments.

Negotiating a Repayment Plan

- The Student Loans Company (SLC) is flexible and willing to discuss and negotiate a suitable payment plan based on your financial situation.

- There is no minimum income requirement to begin repaying the overpayment, unlike regular student loan repayments, which have an income threshold.

So, in summary, you have options to repay the overpayment, either by having it deducted from future loan disbursements or by setting up a customised repayment plan with the SLC, regardless of your current income level.

The key is to communicate with the SLC to find a manageable solution proactively.

Structuring a Student finance overpayment repayment plan

If repaying the student loan overpayment in a lump sum is not feasible, you can negotiate a repayment plan with the Student Loans Company (SLC).

The SLC is generally open to discussing your specific circumstances and making suitable arrangements.

As long as you are reasonable in your approach, there is no need to be concerned when working with the SLC. However, if you feel the SLC is not providing sufficient assistance, you can explore other options for additional support.

The key is to proactively communicate with the SLC and be willing to find a manageable solution together.

By setting up a customised repayment plan, you can avoid the stress of a one-time repayment and work towards clearing the overpayment at a pace that aligns with your financial capabilities.

What happens if you don’t repay your student loan overpayment?

Failing to address your student loan overpayment can result in significant stress and complications. If you neglect to repay the overpayment, the Student Loan Overpayment Debt Collection department will reach out to you.

If you continue to ignore their communications, the debt collection process will officially commence.

Curious about how this process works? Let’s explore it further.

Debt Collection Procedures: What happens if you don’t repay your student loan overpayment?

If you continue to ignore letters from the Student Loan Overpayment Debt Collection department, the situation can escalate quickly.

It is crucial to maintain communication with the Student Loans Company (SLC) from the moment you receive your first notice.

If you persist in ignoring their communications, the SLC may enlist a debt collection agency to recover the owed funds.

The debt collection process can unfold in two primary ways:

- Internal Collection: The SLC may use its agents to collect the outstanding amount.

- External Collection: Alternatively, the SLC might hire a debt collection agency, such as Cabot Financial, to pursue the recovery of your overpayment debt.

Eventually, if you continue to disregard their attempts to contact you, the SLC may become frustrated and decide to take legal action.

They could seek a County Court Judgment (CCJ) against you, which would legally obligate you to repay the overpayment if the court rules in their favour.

Could the situation worsen? Yes, it can, and here’s how.

The Possibility of Student Loans Employing Bailiffs

If you continue to disregard debt collection efforts, there is a possibility that bailiffs may become involved.

In this scenario, the Student Loans Company (SLC) would need to return to court to obtain a warrant or writ that allows enforcement agents (bailiffs) to visit your home and seize your belongings if you ignore initial court orders.

The seized items would be stored and eventually sold at auction to recover the debt. After settling the student loan overpayment, any remaining balance will be returned to you.

This situation can indeed be alarming, but it is a harsh reality: bailiffs can be employed to recover debts related to student loan overpayments.

So, what ultimately happens to these loans? Let’s find out.

Understanding if Student Loans Can Ever Be Cancelled: Does student debt ever get written off?

Did you know that student loans can be written off after a certain period? For instance, Plan 1 student loans are forgiven after 25 years.

However, it is less clear whether a student loan overpayment debt can be considered statute-barred and thus cleared after six years.

Generally, the prevailing belief is that student loan overpayments do not qualify for cancellation under statute-barred status.

Understanding Your Legal Protections When Dealing with Debt Collectors

Dealing with debt collectors can be overwhelming, but it’s important to remember that they do not have the same rights as bailiffs. You have numerous legal protections when it comes to managing your student loan overpayment debt.

Get help with your student loan overpayment.

If you’re struggling to maintain essential living standards while repaying this debt, seeking assistance is crucial.

For additional support, you can reach out to your education provider or the Student Loans Company (SLC).

It’s vital not to ignore communications from the SLC regarding overpayments, as doing so could escalate the situation and make it more difficult to find a resolution.

Contact Details of Student Loans Company

| General Enquiries | 0141 306 2000 |

| Student Loans Company Address | 100 Bothwell StreetGlasgowG2 7JDUnited Kingdom |

| Media Enquiries Email | [email protected] |

| Registered in England No | 2401034 |

| VAT registration number | 556 4352 32 |

| Customer Compliance | 0300 100 0059 |

FAQs

What should I do if I have already paid my student loans on time?

Congratulations! If you have paid off your student loans on time, you are in a great position. Ensure you obtain confirmation from the Student Loans Company (SLC) that your debt balance is zero.

If you haven’t received this confirmation, request a written document from them. If you receive a notice regarding an overpayment, it could be an error, so it’s best to contact the SLC immediately for clarification.

Do I have to pay back my student loans even if I am leaving the UK?

Yes, you are legally obligated to repay your student loans, regardless of your location. The SLC will find ways to contact you, even if you move abroad. They also handle international repayments, so make sure to inform the SLC of your new circumstances and provide them with your updated contact information.

Can student loans be paid back?

Absolutely! Student loans are intended to be repaid. Repayment typically begins after you graduate and your income exceeds a certain threshold. If you have overpaid your student loan, you are also required to repay that amount.

Can student loans be deleted?

Student loans can be written off under specific conditions, such as if you become permanently disabled or after a certain number of years, like 25 years for Plan 1 loans. However, overpayments generally cannot be written off and must be repaid.

What happens if I ignore student loans in the UK?

Ignoring student loans or overpayment notices can lead to serious repercussions. Initially, you will be contacted by the Student Loan Overpayment Debt Collection department. If you continue to ignore their attempts, debt collection agencies and, in extreme cases, bailiffs may become involved.

Is it illegal to not pay student loans in the UK?

While it is not technically illegal to fail to pay student loans, it can result in severe consequences. Not repaying your loans can lead to debt collection processes, and if you continue to ignore the SLC, they may take legal action through debt collection agencies.

What percentage of UK students pay back their student loans?

Estimates suggest that only about 30% of current full-time undergraduates who take out loans are expected to repay them in full. These statistics can change based on various factors, including future income trajectories and changes in loan terms.